No, the 'value' of the club does not have level of debt deducted from it, you're talking about 'profit' in case of sale.

Value = approx. 12.5X EBITDA

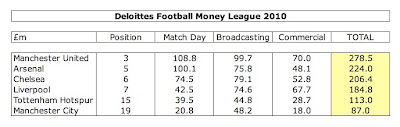

I assume Liverpool is being undervalued due to the desperate circumstances surrounding the sale.

.

The point I am trying to make here is that the club's actual value on the market can only be determined by that market. Forbes thinks fair valuation is 12x EBITDA. Liverpool's new owners think its more like 8.5 x. Maybe that's because of their predicament - maybe that's fair market value for a football club at present - even a high profile one.

The relevance of all this is why do the Glazers want to keep United despite a high level of debt and minimal return for them right now together with considerable hostility from a vocal element of fans?

Assuming that the club is "valued" at £1 bn and that was deemed fair market value. In other words offers are unlikely to exceed that amount. The Glazers would receive approximately £480m

after deducting the bond debt of £520m. With that they have to pay off the PIK debt (£220m) which leaves them £260m to walk away with. Compared to an initial investment of say £275m in 2005 - a not very attractive proposition. Even an offer of £1.2bn would not seem a very enticing propostiion.

Set against that is the prospect of keeping the club and hoping that its revenue growth will continue in the future with costs contained. IN that case, projecting forward to 2017, and assuming 10% per annum growth, revenues will reach £567m with EBITDA at £195. If we then take the 12x multiple the club will be worth 195 x 12 = £2.34bn. If we take the 8.5 x multiple, then the club will be worth £1.67bn.

If the debt is left unrepaid the Bond will be £520m and the PIKs will have ballooned to £631m - giving a total debt amount of £1.15bn. So if the Glazers sold then they would get £1.19bn or on the lower valuation £520m - a big difference.

There is little doubt, therefore, that they will liquidate the PIKs as quaickly as they can and let the bond debt take care of itself. If they can make provision from cash reserves to repay the bond holders, then all well and good.

All the above assumes that revenues continue to grow at the same rate experienced over the past five years, with costs contained. The problem arises in providing for the team, without whose on going success, the above scenario might be difficult to achieve as well as liquidating the PIK debt and paying themselves something on top of that.

It seems high risk but obviously to them a risk worth taking, bearing in mind the success already achieved, both on and off the pitch and the confidence placed in the on going stewardship of the esteemed mananger and competent CEO.

My concern remains that to keep the team really competitive in order to keep revenues growing, there will need to be significant expenditure outlayed on it over the next few years. That should have started already but because of concerns about costs, such expenditure has been limited to what I call a few "young hopefuls".