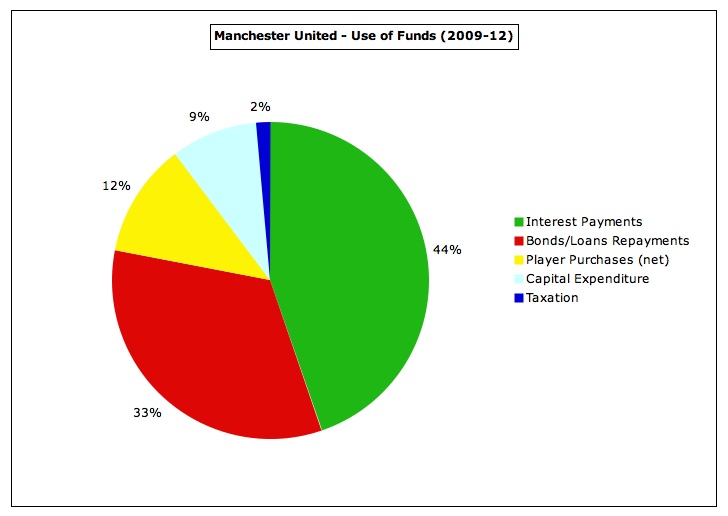

I'm assuming that you're not referring to our on-field performance as a "mess" (5 Prems and two 2nds in the last 7 years together with 3 CL finals, a WCC and sundry cups and shields), so you must be talking about the financial side. Hopefully you understand that mssrs Harris, O'Neill, Green and Drasdo were hell bent on making things look as bad as possible. The "550 mill" figure is an artifact of this. It's easiest to get at the reality by looking at cash flows in and out of the club over the 7 years from 2005 to 2012.

Total revenue: 1,856.144 mill

Player sales: 177.847 mill

Total Cash Inflow: 2,033.991 mill

Staff costs: 878.898 mill

Operating expenses: 384.397 mill

Net fixed assets: 89.561 mill

Player purchases: 294.867 mill

Total Cash Outflow: 1,647.723 mill

Difference: 386.628 mill

The "Difference" figure is essentially the operating surplus generated by the club. If we were still a plc both taxes and dividend would be paid out of that surplus. I estimate that the total of taxes and dividends over the period would have been around 240 mill; Green estimates the figure to be closer to 190 mill. In a spirit of compromise I'll split the difference and assume 215 mill. That leaves 171 miil that we have to account for. 5 mill went to increasing our cash reserve, so we are left with 166 mill that the Glazers are responsible for - not a small amount, but not 550 mill.

There are a couple of further twists to this story. There's an assumption hidden in there that, if we had continued as a plc, we would have generated the same revenues and, in particular, that the same growth in Commercial revenues would have occurred - even Green (andersred) has given up claiming that as likely. If the plc would have generated less revenue, the "cost of the Glazers" goes down from the 166 mill. But that might not be the most important impact.

The plc was wedded to the rule that player costs should be less than 50% of revenue. Without the immediate increase in commercial revenues - the shift to AIG and the increase in other sponsorships - that occurred after the LBO, salary growth would not have been possible within the constraint. In particular, it seems likely that we would only have been able to sign two of Evra, Vidic and Carrick - oops. Of course we'll never know what would have happened, but it's not inconceivable that a significant element of our on-field success was dependent on the growth of commercial revenues, and who knows what SAF would have done if he felt the board was not supporting him. Anyway, it's a good story and, before we get too busy condemning the Glazers, I suspect that a glance at the bigger picture might not be a bad thing. Blood sucking leeches vs. the saviours of our team????????????

Good messaging that! We need to move the argument on from: Blood sucking leeches vs. maybe they aren't too bad. Good thinking!

You need to be a little more careful about preserving the appearance of impartiality though; "I can't get the "Glazer cost" down below 40-50 mill no matter how bad I assume the plc might have been." just doesn't read well.

As for your dilemma, you just need to try harder! You could always conjure up an even worse worst case scenario for the counterfactual plc (but without ever going into specifics) or alter your "great analysis" above to include a

few more "Difference" friendly errors.

For Hell's sake, don't make errors that are counterproductive- your "Net fixed asset" figure is too low. And you have excluded cash pay exceptional expenses, a not insignificant sum over the 7 year period. That omission works against what you're trying to accomplish- reducing the "Difference" figure.

You have excluded the positive working capital movement over the period. Good. That reduces "Total cash inflow" by about 90m and hence reduces the "difference" figure by the same. Nicely done.

My only worry though is that someone in the habit of reading financial statements might spot some of the errors\omissions above and pooh-pooh your "great analysis".

For instance:

1) They might argue that your quaint cash flow method is nonsense as it leaves out important elements, elements that actually need to appear in a proper explicit cash flow working.

2) They might observe (from the actual accounts) that total interest and debt repayment during the period was in excess of 410m and that excludes the dividend payment of 10m (and some other bits 'n' bobs). That contradicts your "Difference" figure of 387m.

3) A resourceful dullard might note that your "Difference" figure should equal [net cash inflow from operating activities - net players - net fixed assets] and demonstrate the weakness of your approach by arriving at a figure of c. 480m for "difference" (while using your incorrect figure for net fixed assets).

4) Any ordinary joe might spot that the increase in cash reserves during the period is a lot more than 5m- another error that works against what you are trying to achieve: reducing the "Difference" figure.

Now, I don't expect any of the above to happen but you can never tell. Publishing a detailed working to support an argument is always risky. It's much safer to eschew details, remain broad-brush, and concentrate on acclaiming the Glazer's commercial expertise.

Like the e-departed GCHQ.